For years, artificial intelligence has been told as a story of unstoppable progress. Every few months, a more powerful, faster, more capable model appears. The feeling is that there is no ceiling.

But there is a less visible reality that is beginning to assert itself strongly: artificial intelligence is not growing as fast as it could. And it’s not due to a lack of innovation.

It’s due to a lack of infrastructure.

Behind every model, every inference, every digital service, there is a physical layer that rarely enters the conversation: data centers. And that layer is starting to show its limits.

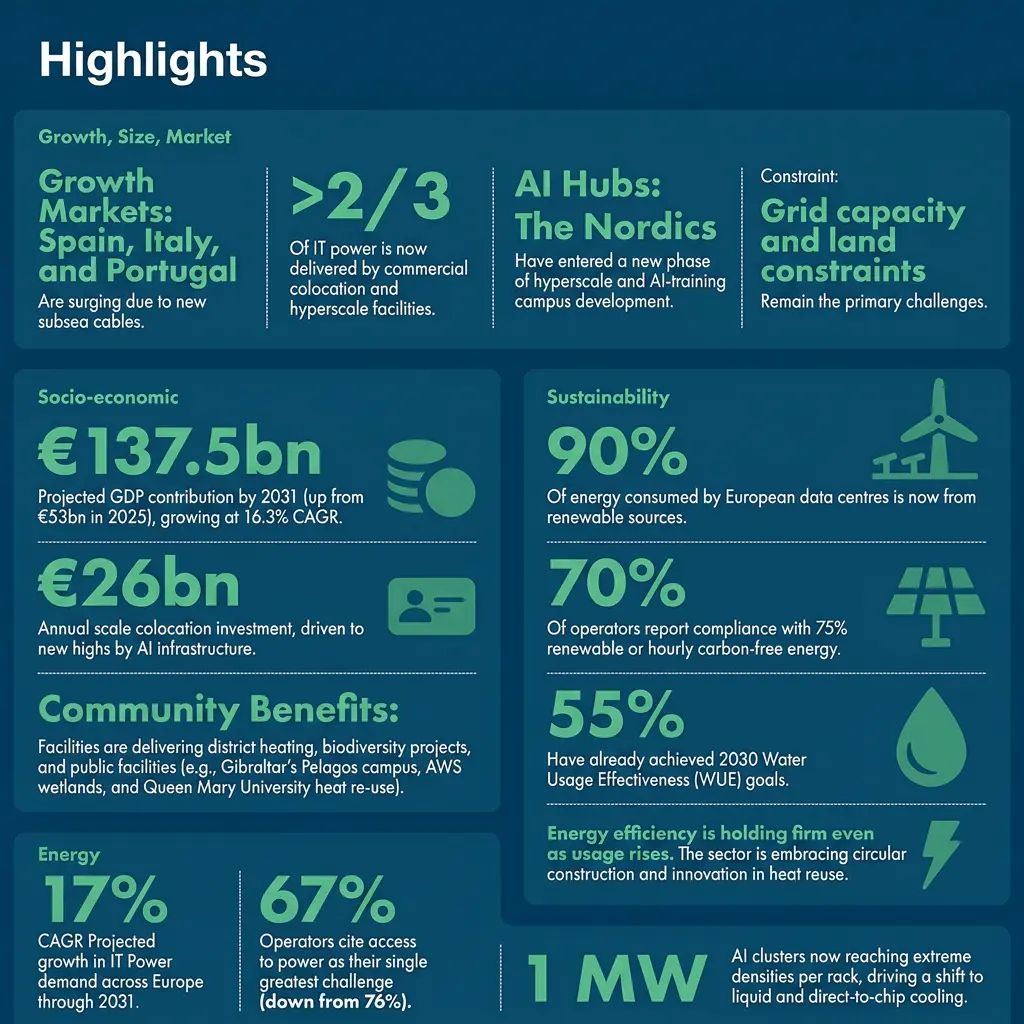

The latest report from the European Data Centre Association paints a revealing picture. The sector is growing at historic rates, driven by the massive adoption of cloud and, above all, by the explosion of artificial intelligence. In just one year, installed capacity in Europe has increased rapidly, approaching growth rates of 20%.

However, that growth no longer depends solely on demand. It depends on something much more basic: energy. The paradox is clear. Never have we had so much technological capacity, yet every new advancement requires a significantly greater amount of energy. Data centers designed for AI do not resemble those of five years ago. They operate with much higher computing densities, require advanced cooling systems, and need completely redesigned electrical infrastructures. And that has consequences.

Today, building a data center is no longer just a matter of investment or market demand; it is a matter of access to energy, network capacity, and regulatory feasibility. In many cases, projects are not halted due to a lack of customers, but because of the inability to connect to the power grid or obtain permits in a reasonable timeframe.

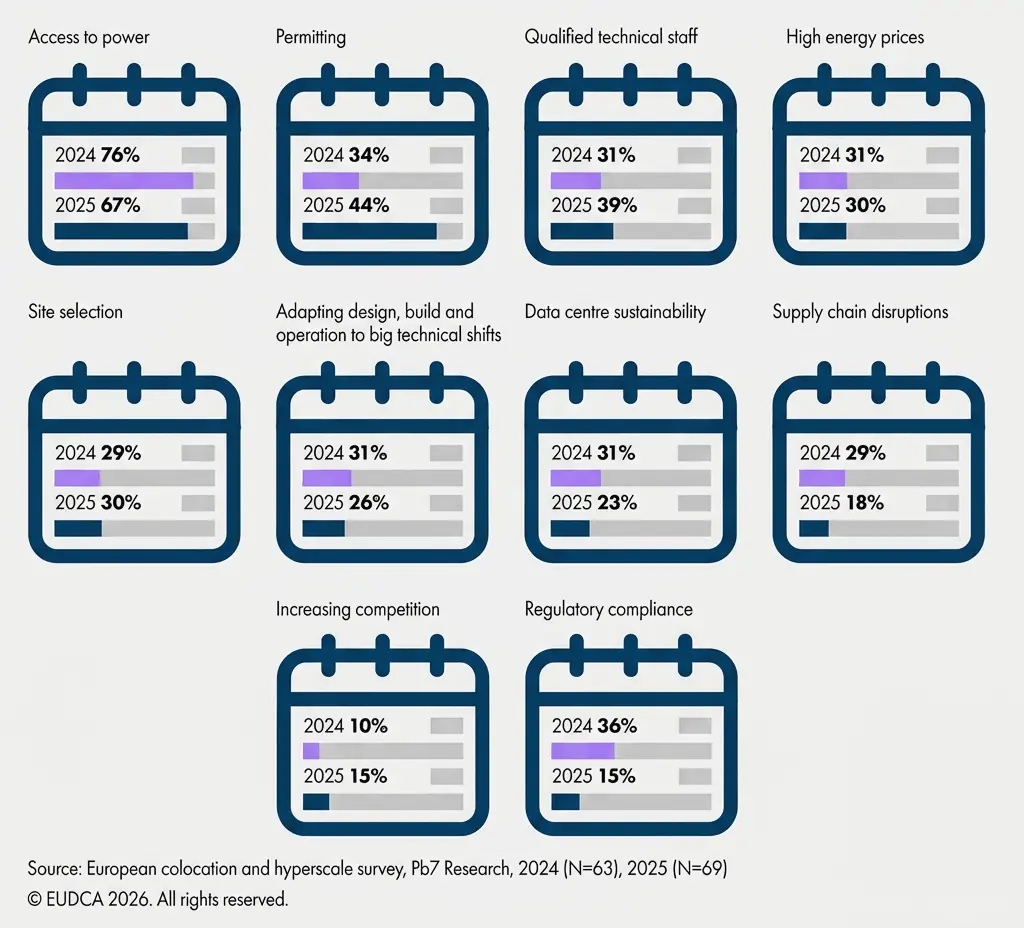

Operators themselves are clear about this. When asked about the main challenges facing the sector, the answer does not revolve around demand or technology, but around much more structural factors.

Question: What are the biggest challenges for your organisation for the next three years? (multiple response, top 10 answers)

Access to energy tops the list by far, followed by permitting processes, talent availability, and energy costs. It is a clear signal that the problem is no longer digital—it is physical. This is changing something fundamental: the digital map.

For years, Europe concentrated its infrastructure in a few major hubs. Frankfurt, London, Amsterdam, Paris, and Dublin acted as the digital heart of the continent. But that model is starting to become insufficient. Pressure on the power grid, land scarcity, and regulatory complexity are pushing growth toward new regions.

Today, data centers are being deployed where energy is available, where connectivity allows it, and where regulatory conditions are viable. The result is a much more distributed Europe, where the north, south, and east are gaining prominence compared to traditional hubs.

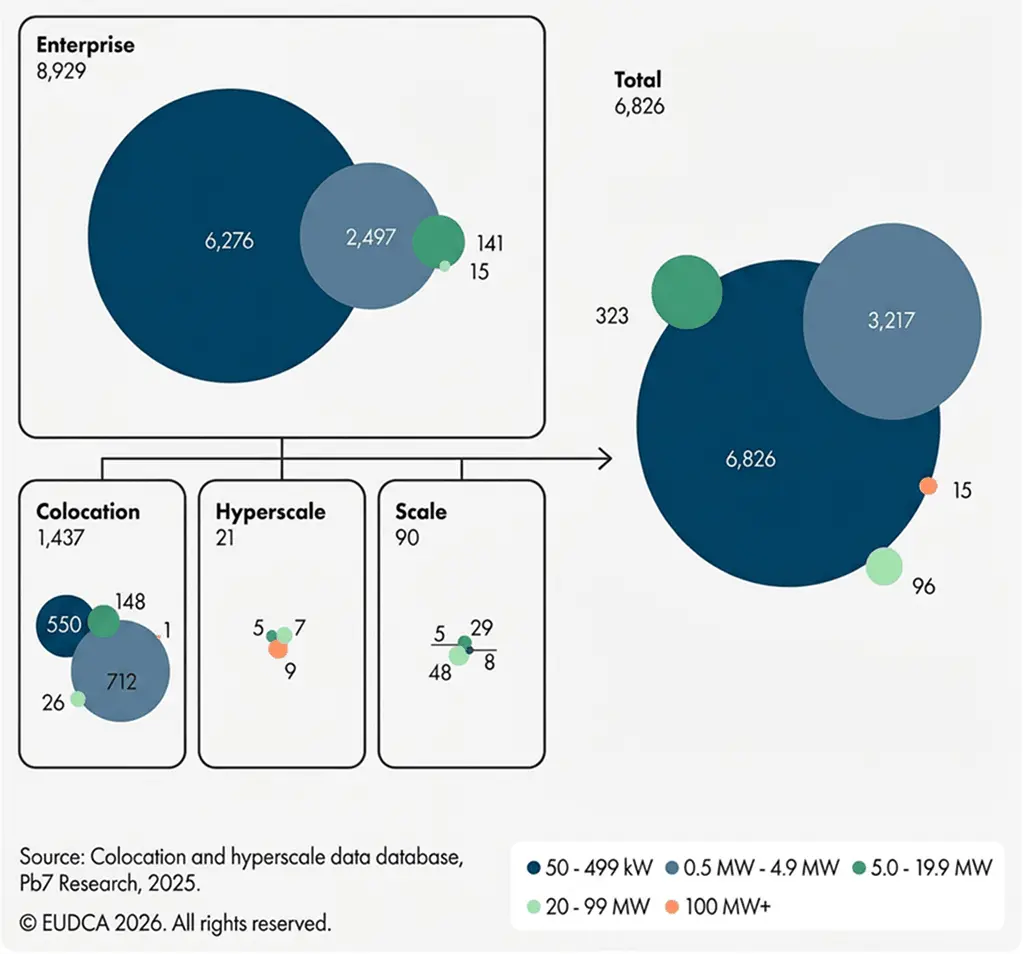

Data centres in Europe by type and IT Power (50 kW or more), 2024

his shift is not only technical, it is strategic.

Because data centers are no longer just technological facilities. They have become critical infrastructure. They are the foundation on which the digital economy is built, but also a key element in terms of sovereignty, security, and competitiveness.

Europe knows this. That is why the debate is no longer only about how to grow, but how to do so without compromising energy supply, without straining resources, and without excessive dependence on external actors. In this context, artificial intelligence ceases to be only a technological challenge and becomes an industrial one.

Growth will not be infinite. It will be conditioned by the ability to build, power, and sustain the necessary infrastructure. And this introduces a new logic into global competition.

It will not be enough to have the best models or algorithms. It will be essential to have access to energy, network capacity, and deployment capability. In other words, the next competitive advantage will not be only digital, it will be physical.

Artificial intelligence may continue to advance at great speed, but its true limit will not lie in the code. It will lie in the real world—in the energy it can consume, the infrastructure that can sustain it, and the ability of countries and companies to build it in time. Because, for the first time in a long while, the future of the digital world depends directly on the physical one.

Source

State of European Data Centres 2026